June 15, 2026|

Cash application is often treated as a back-office accounting function. In reality, it is one of the most important control points in the order-to-cash cycle.

When payments, remittances, short pays, deductions, chargebacks, discounts, and customer references are not captured and matched quickly, every downstream A/R process suffers. Collections teams work from outdated balances. Credit decisions are based on incomplete account data. Deduction teams lose time gathering backup. Finance lacks clear visibility into cash, disputes, and revenue leakage.

The goal of modern auto-cash application is not simply to post payments faster. The goal is to create a clean, auditable, daily view of cash, open A/R, exceptions, and deductions so the business can act with confidence.

Why Cash Application Is More Complex Than It Looks

In a perfect world, every customer would pay the exact invoice amount and provide clean remittance detail in a standard format.

That is rarely how B2B payments work.

A single payment may cover hundreds or thousands of invoices. Remittance data may arrive separately by email, EDI, portal download, spreadsheet, PDF, lockbox image, or customer statement. Customers may short pay for discounts, freight, shortages, returns, trade promotions, pricing claims, compliance chargebacks, or unauthorized deductions. Parent-child account relationships, multiple ship-to locations, customer-specific deduction codes, and missing invoice references add another layer of complexity.

Manual cash application can manage this at low volume. At scale, it becomes slow, expensive, and difficult to control.

Best Practice 1: Capture Every Remittance Source

Auto-cash performance depends on data capture. The system must be able to ingest and normalize remittance detail from all common sources, including:

- Bank files and lockbox images

- ACH, wire, check, and EFT remittance data

- EDI 820 files

- Customer emails and attachments

- PDFs, spreadsheets, CSV files, HTML files, and images

- Customer and retailer portals

- ERP and customer master data

The stronger the intake process, the less work is pushed to manual exception handling.

Carixa® CashApply is designed to capture remittance detail across formats and sources, then normalize that information for matching, posting, and downstream workflow.

Best Practice 2: Match Beyond Invoice Number

Invoice-number matching alone is not enough.

Modern cash application must use multi-factor matching logic, including:

- Customer account and parent-child relationships

- Invoice number

- Purchase order number

- Payment amount

- Open balance

- Due date

- Customer account number

- MICR and bank account data

- Credit memo references

- RMA or return authorization numbers

- Customer deduction and reason codes

When remittance information is incomplete, alternate matching criteria become essential. This is where rules, algorithms, historical behavior, and machine learning can reduce repetitive manual handling. Intelligent document processing can automatically extract remittance information from PDFs, emails, lockbox images, and spreadsheets before matching begins.

Best Practice 3: Separate True Exceptions From Routine Variances

Not every variance deserves the same treatment.

Small discounts, freight differences, tax issues, pricing variances, shortage claims, chargebacks, and trade deductions should not all land in the same unresolved bucket. A strong auto-cash process applies tolerance rules, customer-specific rules, deduction coding, and routing logic so that each item moves to the right next step.

That may include:

- Automatic posting

- Tolerance write-off under approved policy

- Creation of a deduction case

- Chargeback to the customer

- Routing to collections

- Routing to deduction recovery

- Routing to trade promotion validation

- Requesting additional backup from a portal or internal system

The purpose is to keep cash moving while preserving visibility and control over unresolved revenue.

Best Practice 4: Connect Cash Application to Deduction Management

Cash application and deduction management should not operate in isolation.

A short payment is often the first signal of a deduction, chargeback, claim, or revenue leakage issue. If that item is simply posted as an unresolved difference, the company may lose valuable time needed to dispute, validate, or recover it.

Carixa connects cash application with deduction workflow so deductions can be coded, documented, routed, and resolved faster. If a customer takes a shortage deduction, the system can trigger documentation retrieval. If a deduction matches an open credit memo, it can be applied. If a trade promotion claim requires validation, it can move into the appropriate workflow.

This turns cash application from a posting function into a revenue control function.

Best Practice 5: Use Portal Automation Where Remittance or Backup Is Missing

Many customers and retailers no longer send complete remittance or backup documentation directly. Instead, critical information sits inside customer AP portals, retailer portals, carrier portals, or deduction portals.

Manual portal work slows down cash application and deduction resolution.

Carixa® PortalExchange helps automate portal access, document retrieval, claim backup capture, and related workflow steps. This is especially important for suppliers dealing with high-volume retail customers, where deductions, chargebacks, and compliance claims may require supporting documents before they can be validated or disputed.

Best Practice 6: Maintain a Complete Audit Trail

Every cash application decision should be traceable.

A strong system should show:

- What was received

- Where the remittance data came from

- How the payment was matched

- What rules were applied

- Who handled any exception

- Why a deduction, write-off, chargeback, or adjustment was created

- What documentation was attached

- When the item was posted or routed

This audit trail supports accounting control, customer dispute resolution, internal accountability, and management reporting. Organizations that periodically review these workflows often uncover recurring process failures that continue generating preventable deductions.

Best Practice 7: Close Cash Daily

Daily cash closing is one of the clearest indicators of A/R process health.

When cash is not applied daily, the impact spreads across the organization. Collectors may contact customers about invoices that were already paid. Credit teams may make decisions using inaccurate balances. Deduction analysts may lose time reconstructing short-pay activity. Finance may lack confidence in open A/R and cash reporting.

Auto-cash application should support the practical operating goal of closing cash every day, with exceptions clearly identified and routed for action.

Best Practice 8: Measure Exceptions, Not Just Posting Speed

Posting speed matters, but it is not the only metric.

Companies should also measure:

- Auto-match rate

- Exception rate by customer

- Exception rate by payment type

- Unapplied cash aging

- Deductions created from short pays

- Discounts taken outside policy

- Recurring reason codes

- Portal-sourced documentation volume

- Manual touches per payment

- Time to clear exceptions

These metrics show where automation is working, where customer behavior is creating cost, and where preventable revenue leakage is occurring.

Best Practice 9: Combine Automation With Experienced Oversight

Automation should handle routine work. Human expertise should focus on exceptions, policy decisions, customer behavior, and recovery opportunities.

The best results come from combining software automation with experienced A/R professionals who understand payment behavior, deductions, trade claims, retailer practices, and customer-specific patterns.

That is the Smyyth model: Carixa automation supported by deep practitioner experience.

Best Practices Summary

- Capture every remittance source.

- Match beyond invoice numbers.

- Automate exception routing.

- Connect cash application with deduction management.

- Automate customer portal processing.

- Maintain a complete audit trail.

- Close cash daily.

- Measure exception trends.

- Combine automation with experienced A/R professionals.

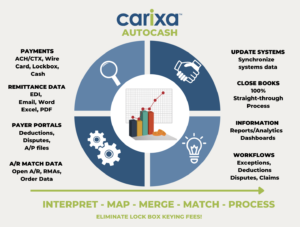

How Carixa CashApply Improves Auto-Cash Application

Carixa® CashApply helps companies automate and control the cash application process across payment types, remittance formats, customers, and ERPs.

Key capabilities include:

- Remittance capture from bank files, EDI, email, PDF, spreadsheets, lockbox images, and portals

- Multi-factor matching across invoices, accounts, purchase orders, amounts, dates, credits, and customer references

- Parent-child account matching

- Exception routing and workflow

- Deduction and chargeback coding

- Integration with deduction, collection, trade promotion, and reconciliation workflows

- Customer-specific rules and tolerance handling

- Auditable posting history

- Reporting on cash application performance, exceptions, and recurring issues

For companies with high transaction volumes, complex customer relationships, or significant deduction activity, automated cash application can improve more than posting efficiency. It can strengthen revenue control across the entire credit-to-cash cycle.

The Bigger Point: Cash Application Is Where A/R Becomes Actionable

Cash application is the moment when payment activity becomes financial truth.

If that process is slow, fragmented, or manual, the entire A/R operation works from imperfect information. If it is automated, controlled, and connected to deductions and collections, the company gains faster cash visibility, cleaner open A/R, better dispute handling, and stronger revenue protection.

Carixa CashApply helps finance teams move from manual posting to daily A/R control.

Learn more about Carixa CashApply, explore the complete Carixa Accounts Receivable Automation Platform, or contact Smyyth to discuss how automation can accelerate cash application, reduce manual effort, and improve revenue recovery.

Contact us at info@smyyth.com for more information.